Pensions

What is tailored drawdown? And how can it help me to pay less tax?

Find out how tailored drawdown could help you to pay less tax on your retirement income.

id

Looking to pay less tax in retirement? Tailored drawdown could be a good way to help you cut back. Find out how it works.

id

When it comes to accessing your pension benefits, there are a few different ways to do it. Once you turn 55 (rising to 57 on 6 April 2028), you can either buy an annuity (a guaranteed income for life), take it as a flexible income (also known as drawdown), take it as one or more lump sums or you could choose a combination of these options.

If you choose to go down the drawdown route, you can sometimes choose an option we call ‘tailored drawdown’, which could help you cut back on the amount of tax you pay. Here’s how it works.

What is tailored drawdown?

Most people will get 25% of their pension savings tax-free and will pay income tax on the remaining 75%. Although keep in mind you’ll only get up to a maximum of £268,275 tax-free, which is a quarter of the lifetime allowance (unless you have lifetime allowance protection for a higher amount).

If you choose to take your money as drawdown – a bit like paying yourself a salary, except you can choose how much to take at a time – you get a bit of flexibility with how much tax-free and taxable income you take from your plan.

Tailored drawdown is basically a mix of the two. That means you can take some of your tax-free lump sum and some of your taxable income at the same time to provide your retirement income.

How does drawdown work?

When you choose drawdown, you decide how much money you want to take and when to take it. You can set up a regular income that you can stop, start or change at any time.

To fully understand how tailored drawdown works, it’s important to first understand how drawdown itself works. We have an article called What is pension drawdown? if you want to deep-dive into it, but here’s a quick summary:

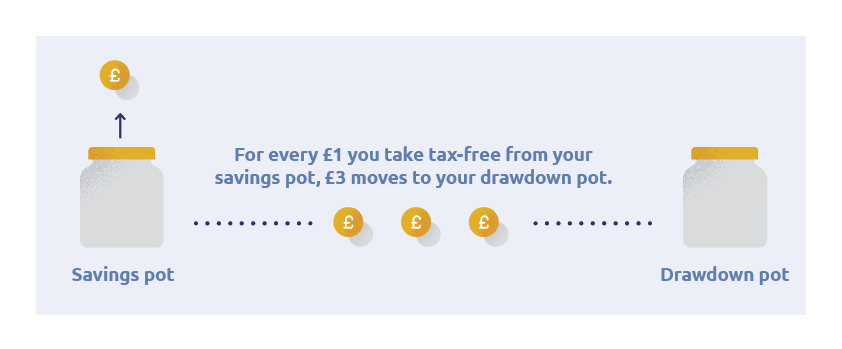

Think of your pension savings as being divided into two pots – your savings pot and your drawdown pot. When you pay into your workplace or personal pension plan, the money goes into your savings pot. You can normally take a quarter of the value of your savings pot as your 25% tax-free lump sum. Meaning for every £4 in that pot, you can take £1 tax-free and £3 as taxable.

We need to earmark the money you’ll pay income tax on. So for every £1 of tax-free lump sum you take from your savings pot, £3 moves to your drawdown pot. The money in your drawdown pot is the money you’ll pay income tax on.

How does tailored drawdown work?

With tailored drawdown, you’ll take a bit from both pots.

Let’s say you’re looking to take £2,000 a month from your pension savings as your retirement income. If you took £1,000 from your savings pot each month (as part of your tax-free lump sum), your pension provider would move £3,000 to your drawdown pot. You can then take another £1,000 from your drawdown pot as taxable income.

It doesn’t necessarily need to be a 50/50 split of tax-free and taxable. But there needs to be enough money in each pot to able to carry out your instruction.

Why is tailored drawdown more tax effective?

Depending on your tax code, you could find that using tailored drawdown means you pay less income tax overall or, in some cases, none at all.

This is because most people will get a tax-free personal allowance, which is £12,570 for the 2023/24 tax year. Income tax is only paid on anything you earn above this.

HMRC will class any taxable income you take from your pension plan as earnings. So if you don’t have earnings from anywhere else, then you’ll usually have this tax-free allowance when it comes to your pension income. Meaning you could take just over £1,000 from the taxable part of your plan (your drawdown pot) every month without actually paying any tax on it at all.

Think of it like a salary from a job. If you were earning £12,000 a year, you’d be under the personal allowance and so wouldn’t have to pay any tax.

It might not be enough to fund your lifestyle in retirement on its own, so this is where the tax-free lump sum comes in. Topping up the amount you already get as your tax-free personal allowance with your 25% tax-free lump sum every month could mean you don’t pay a penny of tax.

Some things to think about

- Because of how pension pots work, you’ll need to have enough money in your drawdown pot to fund the amount of taxable income you want to take.

- With both drawdown and tailored drawdown, any money you don't take stays invested, which means its value can go down as well as up. How much money you take, when you take it and how your investments perform will affect how long your pension savings last for. You need to manage your investments and withdrawals to make sure your savings last as long as you want them to.

- Keep in mind that taking taxable income from your plan will reduce the amount you can pay in to £10,000 a year – known as the money purchase annual allowance.

- The amount of income tax you pay on your pension savings will depend on the tax code held against your plan (which is provided by HMRC).

- Make sure to check that your pension provider offers tailored drawdown as not all providers will have the product available to facilitate this. It's important to shop around. Other providers may offer a better retirement income, and options more suited to your circumstances.

- We recommend you get guidance or financial advice before making any decisions. From age 50, you can get free impartial government-backed guidance from Pension Wise, a service from MoneyHelper. You can find out more on their website or call 0800 138 3944.

id

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.

A pension is an investment, the value can go down as well as up and you could get back less than you paid in.

The information here is based on our understanding in August 2023 and shouldn’t be taken as financial advice.

Related Articles

-

Is it time to consolidate your pension?

Confused about whether to combine your pensions? It's a decision many people struggle with. Here’s how to decide what’s right for you. MoneyPlus Features Team

MoneyPlus Features TeamJuly 30, 2026

Read more6 mins read -

Pension investment 101

Pensions don’t work like traditional savings accounts. They’re invested with an aim to grow your money so you could have more in retirement. Find out how.

MoneyPlus Features TeamJuly 29, 2026

Read more4 mins read -

Can you trust AI with your finances?

Many people use AI tools to help with financial planning. If you're one of them, learn the benefits and limitations of these tools and how to use them safely.

MoneyPlus Features TeamJuly 29, 2026

Read more4 mins read