A self-employed pension built for you

Our Personal Pension is a great option for self-employed people and directors of limited companies:

- Quick and flexible

Apply in minutes. Manage online or in our app. - Tax is sorted for you

Get basic rate tax relief automatically. - Open with £1

Top up, pause, or change payments whenever you like. - UK based support

Our pensions experts are here to help you.

Who's it for?

- Sole trader or freelancer

- Director of a limited company

- Other savers who want a simple, flexible pension

How tax relief works

We keep things simple. We'll automatically claim 20% tax relief to top up every payment you make. So for every £80 you pay in, £100 will go into your pension. Higher and additional rate taxpayers can apply for extra tax relief on their tax return.

Company director? Business contributions are deductible from your corporation tax bill.

Call us on 0800 634 7476 to set this up.

Our tips for company directors.

Laws and tax rules may change in the future. Your own circumstances and where you live in the UK will have an impact on tax treatment. Call charges will vary.

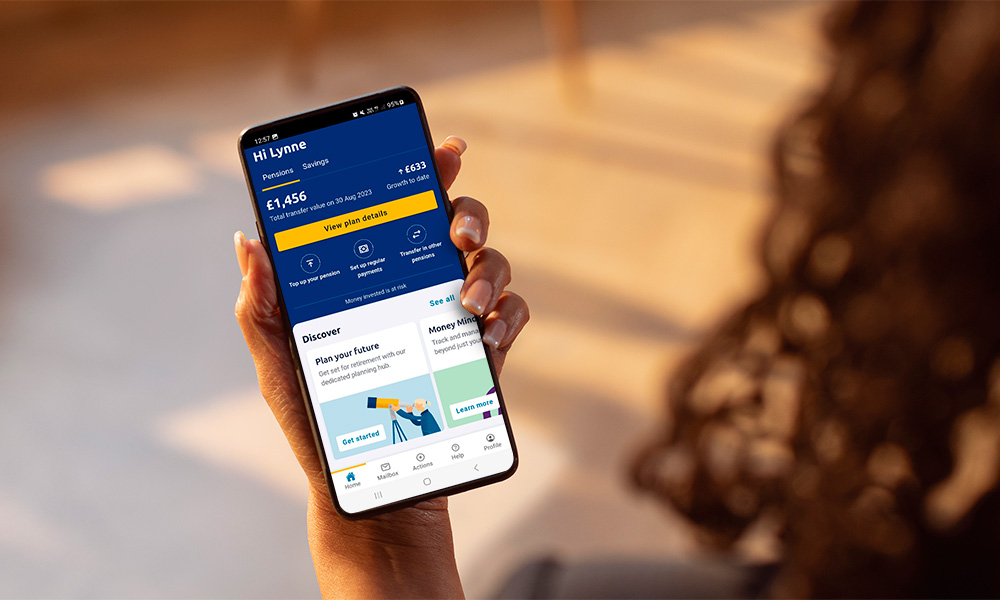

Pensions to transfer? It’s easy

Having one pension gives you a clearer picture.

It’s easy to transfer now or later. All you need is the provider name, policy number, and a rough estimate of the value.

Transferring may not be right for everyone.

Self-employed pension FAQs

More about our personal pension

-

Our charges

-

Investment options

-

Paying in

-

Accessing your pension