Pensions

What is pension drawdown?

Pension drawdown, also known as income or flexi-access drawdown, is a way of taking money out of your pension pot while leaving the rest invested. Find out how it works.

id

When you reach retirement, pension drawdown will be one of your options to access the money in your pension pot. Here we explore what it is, how it works and the key things you need to think about before taking the next step.

What does ‘pension drawdown’ mean?

Pension drawdown is a retirement option that lets you take some money out of your pension pot at any time from age 55 (or 57 from 6 April 2028), while you leave the rest invested. It’s also sometimes referred to as income drawdown or flexi-access drawdown.

You have complete control over how and when you take your money out. You can set up regular withdrawals – which you’re free to stop, start or change at any time – or you can take cash lump sums whenever you need them. You can even choose to enjoy a combination of both.

You’ll normally be able to take up to 25% of your total pension savings tax-free, up to a maximum of £268,275. And you can take that allowance as one big lump sum, or spread it out over a few smaller tax-free withdrawals. You could even decide to take an income that’s made up of both tax-free and taxable elements.

How does pension drawdown work?

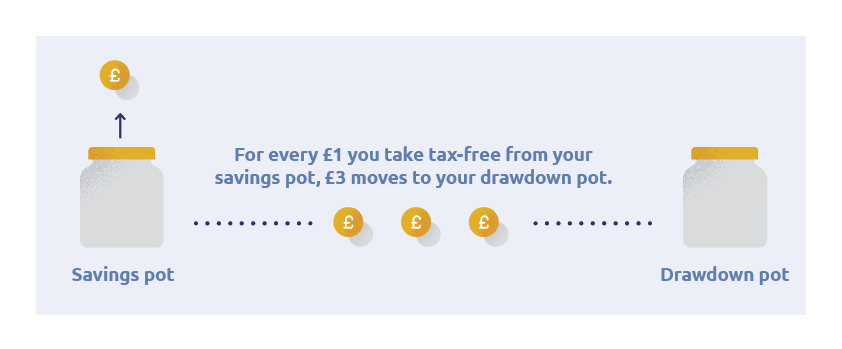

When you go into drawdown, your provider will split your pension pot into a drawdown pot and a savings pot. This helps to track and manage your tax-free cash entitlement as you take money out, but still gives you the option to put money into your pension (if that’s what you’d like to do).

In simple terms, up to 25% of any money you have in your savings pot can be paid to you tax-free. Anything you have in your drawdown pot will be classed as taxable income when you access it.

To make sure you stay within your tax-free allowance, your provider will automatically move £3 into your drawdown pot for every £1 you take tax-free from your savings pot. The £1 represents the 25% that’s tax-free and the £3 represents the remaining 75% that will be taxed as income at your marginal rate when it’s paid.

id

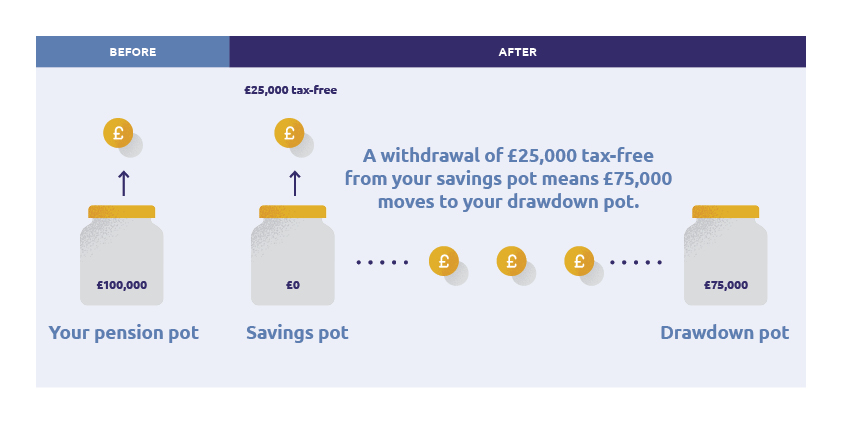

To bring this to life, let’s assume you have £100,000 in your pension pot. We can then look at a couple of examples of how you might take your tax-free cash entitlement – and how this will guide what happens in both your savings and drawdown pots.

1. Take all your tax-free cash in one go

From your £100,000, your provider would pay you a £25,000 tax-free lump sum (making up your full 25% tax-free allowance) from your savings pot. They’d then move the £75,000 you have left over into your drawdown pot. This would then be taxed as income at your marginal rate at the point you come to access it. Don’t forget, your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.

With this option, you’ll have fully used up your tax-free allowance under this plan – unless you chose to pay more money into your savings pot.

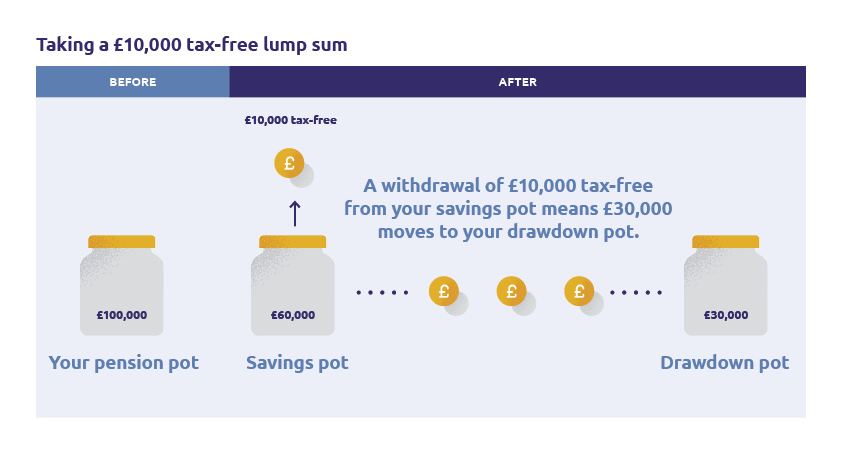

2. Take a series of smaller tax-free withdrawals

Rather than taking all your tax-free cash as one big lump sum, you could choose to take your allowance over a series of smaller chunks.

So say you only wanted to take a £10,000 tax-free payment, your provider would only move £30,000 into your drawdown pot (remember £3 for every £1 you take out tax-free will be moved here).

This would leave you £60,000 untouched in your savings pot – which you could still take a 25% tax-free payment from at a later date.

Benefits of pension drawdown

There are various benefits to pension drawdown. When it comes to accessing your pension savings, this option can offer a lot of flexibility, as you’re in control of how much money you take and when you take it.

And any money left in your pot stays invested. Generally, the longer your money is invested, the more opportunity there is for it to grow, thanks to a process called compounding. Keep in mind a pension is an investment. Its value can go down as well as up and could be worth less than was paid in.

What happens when you die?

If you die and there’s still money left in your plan, it can be passed on to your beneficiaries. They can choose to take it as a lump sum, or have it paid to them as pension drawdown. Remember to keep your beneficiaries up to date so your pension provider knows who you want your pension savings to go to. If you're a Standard Life customer you can do this online or by calling us. If you want to find out more about our online services, you can take a look at our website.

If you were to die before you reach age 75, these payments would be completely tax-free (regardless of whether the money is sitting in your savings pot or your drawdown pot). If you die after you reach age 75, any payments would be taxed at your beneficiary’s marginal rate.

Potential risks of pension drawdown

Just like any of the other ways you can choose to access your pension savings, there are risks that come with drawdown.

One of the big ones is that, unlike with a pension annuity, your future income isn’t guaranteed.

Your pension savings will remain invested in the stock market. And while this can give them the chance to grow, it also means you could see them drop in value too.

At the same time, if you take out too much money too quickly, there’s a chance that your savings could run out before you die. And with one in four men aged 65 today potentially living until they’re 92, and 94 for women, you may need them to last for a very long time.

To help balance these risks, drawdown needs careful planning and ongoing reviews. Keeping a close eye on the performance of your investments, as well as how much money you’re taking out, can help you make sure your income is sustainable. Seeking professional help from a financial adviser to keep on top of this would be recommended.

Think carefully before doing anything

As always, how you choose to access your pension savings is a big decision. It’s important you take the time to understand all your options.

If you do decide you’d like to go into pension drawdown, it’s equally important to shop around so you can get the best deal. You should also be mindful that not all providers will offer the same product features, so make sure you pay close attention to what they will and won’t allow when it comes to accessing your money.

If you’re still unsure or need a bit of extra help, we’d recommend seeking guidance or talking to a financial adviser. If you don’t already have one, you can find a financial adviser at Unbiased.

The information here is based on our understanding in June 2023 and shouldn’t be taken as financial advice.

A pension is an investment, the value can go down as well as up and you could get back less than you paid in.

Standard Life accepts no responsibility for information in external websites. These are provided for general information.

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.