Pensions

How much tax will I pay on my pension withdrawals?

Find out how much tax you’ll need to pay on your pension withdrawals depending on how you take your money and discover whether you’ll pay tax on your State Pension.

id

How much tax you’ll pay when you withdraw money from your pension plan depends on various things – including how you take your money. We look at the ways you can withdraw your pension savings and what the different options could mean for you tax-wise.

You can normally access your pension savings from age 55 (rising to 57 from 6 April 2028). It’s important to know how your withdrawals are taxed so you don’t end up paying more than you need to. We explain more in this article, and you can explore more in our guide on tax on pension savings and tax in retirement.

How much of my pension pot is tax-free?

You can usually take 25% of any pension pot as a tax-free lump sum. You can find out more about taking your tax-free lump sum in our article.

The remaining 75% will normally be taxed in the same way as income you’d get from working. So the amount you pay will depend on what tax band you’re in.

Your tax band is based on your total annual income. This can include money taken from your pension savings; other savings and investments; your State Pension; earnings from work; and certain benefits. You can check your income tax band on the government’s website. Remember, income tax bands are different in Scotland.

And don’t forget, you’ll have a personal allowance, which is the amount of annual income you can have that you aren’t taxed on. For most, this is £12,570 in the current tax year.

How much tax will I pay on a pension in drawdown?

When you take a flexible income (drawdown), how much tax you pay depends on your tax band.

If you choose this retirement option, you can set up a regular income, which you can start, stop or change whenever you want. You can also make one-off withdrawals.

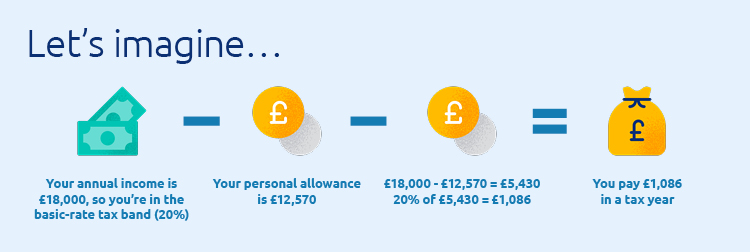

Let’s imagine you’ve set up a regular income that gives you £18,000 a year and that this is your only income. In this case, you’d be in the basic-rate tax band, so you’d pay tax on your pension withdrawals at a rate of 20%. And if you have a personal allowance of £12,570, you’ll pay the 20% tax on only £5,430, rather than £18,000. So you’d pay £1,086 in tax, which would normally be deducted automatically by your pension provider.

id

You might be subject to emergency tax at first, meaning your pension provider might deduct more tax than you actually owe from the first payment they make to you. You’ll need to claim any tax you’ve overpaid back from the government.

But after this first payment, the government will update your provider with your correct tax details. So any taxable withdrawal you make after the first should be taxed correctly.

If you make a one-off withdrawal but don’t take all of your pension pot, you may want to reclaim tax using a P55 form. Even if you don’t actively claim your tax back, the government will normally still refund you if you’ve overpaid. You just might have to wait until after the end of the tax year.

How much tax will I pay on a pension lump sum?

If you take more than 25% of your pot, you’ll pay tax on lump sums based on your tax band.

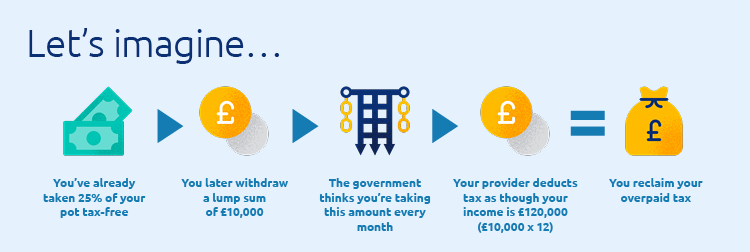

When you first withdraw a taxable lump sum, you’ll probably be put on an emergency tax code. Basically, the government might treat the amount you’re taking as though that’s what you’ll take every month. So if you take £10,000, your pension provider may automatically deduct tax as though your annual income is £120,000.

In this situation, you can fill out a P55 form to reclaim overpaid tax if you haven’t taken all of your pot in one go.

id

Once the government has given your provider up-to-date tax details for you, you should be taxed at your normal income tax rate for future withdrawals.

How much tax will I pay if I take my full pension pot?

If you take your full pension pot in one go, 25% will normally be tax-free, and the rest will be taxed based on your tax band. If you’re taking all your pot in one go, you might have a large tax bill for that year. The more money you take, the more there is to pay tax on.

You might be on an emergency tax code at first. If this results in you overpaying, you can claim tax back. Use a P50Z form if you’re not working, aren’t expecting to go back to work soon, and don’t have other taxable income. Use a P53Z form if you do have other income.

If you have a personal pension pot worth less than £10,000, you might be able to withdraw it in one go as a ‘small pot lump sum’. There are slightly different rules for these. But when it comes to tax, you’ll still get 25% of your pot tax-free, and the rest will still be taxed as income.

Everyone who takes a small pot lump sum will be taxed at the basic rate of income tax (20%). You might not be in the basic-rate tax band, though, so 20% could be more or less than what you actually owe. If you end up overpaying, you can claim tax back with a P53 form.

How much tax will I pay on my pension annuity?

If you buy a guaranteed income for life (annuity) with some or all of your pension savings, you’ll be taxed according to your tax band. Remember, you can normally still take 25% of your pot as a tax-free lump sum if you wish.

You might be on an emergency tax code initially. But once the government has updated your provider with your correct tax details, your provider should pay back any overpaid tax without you having to reclaim anything. And you’ll be taxed at your normal rate of income tax going forward.

Do I pay tax on my State Pension?

Your State Pension is taxable, but tax normally won’t be taken from your State Pension itself.

The full new State Pension is just over £10,600 in the current tax year, which is less than the personal allowance. So this won’t be taxed, but it does count as part of your total annual income.

Imagine you get the full new State Pension, then you take £10,000 as a flexible income from your pension plan in a tax year. Your total income would be over the personal allowance, and you’d pay tax at a rate of 20%. This would usually be deducted from withdrawals from your pension plan, rather than your State Pension.

Learn more about tax and your retirement options

Since money you take from your pension plans is classed as income, it can push you into a higher tax band, particularly if you have other income. Your pension savings may be especially likely to push you into a higher tax band if you’re taking large lump sums or your whole pot.

If you overpay or underpay tax for any reason, the government will get in touch with you at the end of the tax year.

If you’re still wondering which retirement option is best for you, you can read more in our guide on withdrawing money from your pension plan.

If you’re over 50 and you’d like to know more about your retirement options, you can get free, impartial guidance from Pension Wise, a service from MoneyHelper.

The information here is based on our understanding in April 2023 and shouldn’t be taken as financial advice.

A pension is an investment and its value can go down as well as up and may be worth less than was paid in.

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.

Standard Life accepts no responsibility for information in external websites. These are provided for general information.