Pensions

Three reasons why it pays to love your pension

Discover three reasons why it just makes sense to show your pension some love.

id

Feeling in the Valentine’s spirit? Here are three reasons why you should show your pension some love.

1. Because your pension and its tax benefits are a match made in heaven

The tax benefits you get from your pension are hard to find anywhere else. Not only do you usually get 25% of your pension pot tax-free, but you also get tax relief on the payments you pay into your pension.

In a nutshell, the government encourages you to pay into your pension by giving you back the money that you would have otherwise paid in tax. How you get this tax relief will depend on the type of plan you have – for example, in some cases, the extra money will go straight into your pension. In others, your pension payment will come off your salary before you pay any tax. But the general idea is the same for everyone.

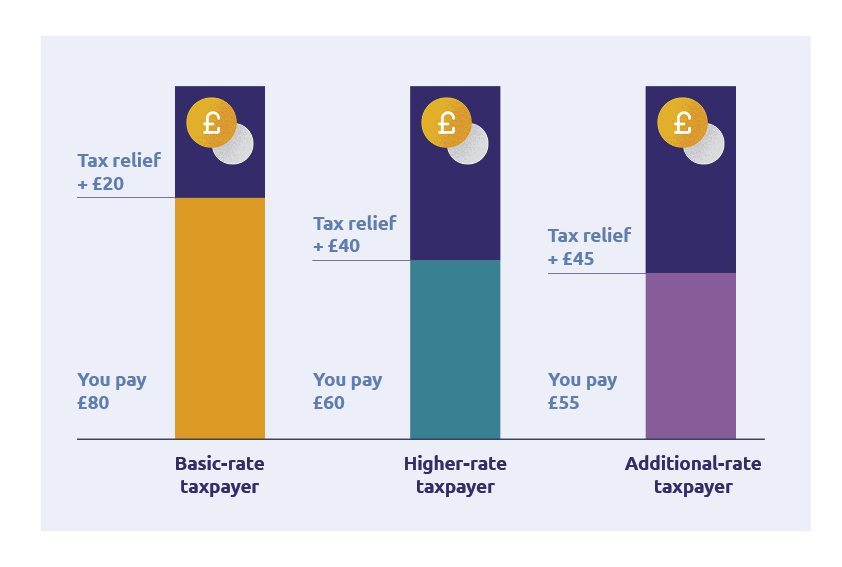

You get tax relief based on the rate of income tax you pay. So, if you pay basic-rate income tax (20%), you’ll get tax relief on your payments for the same amount. Meaning it’ll only cost you £80 to pay £100 into your pension.

If you’re a higher-rate or additional-rate taxpayer who pays 40% or 45% in income tax, it’ll cost you even less. A £100 payment would only cost £60 for a higher-rate taxpayer and £55 for an additional-rate taxpayer.

id

Remember income tax bands are different in Scotland. And keep in mind the extra boost isn’t always automatically applied for higher or additional-rate tax relief, so you might need to claim it back.

2. Because you’re not the only one showing it some interest

If you’ve been automatically enrolled into a workplace pension through your job (which most people will have been), then your employer pays into your plan too.

They need to pay in at least 3% of your qualifying earnings – that’s anything between £6,240 and £50,270. And, in some cases, they’ll pay in more or offer to match your payments up to a certain percentage as an employee benefit.

But if you opt out of your workplace pension scheme, or don’t take your employer up on their benefits, you could be missing out on a big chunk of income when it’s time to retire. So take the time to brush up on what your employer offers and make the most of anything you can.

3. Because if you don’t love it, you could lose it

Had a few jobs? Then you’ve probably got a few pensions too. It’s easier than you think to lose track of old pension plans. Every time you get a new job, a new one is opened for you. And if you don’t keep tabs on the old one, it can be forgotten about.

If this has happened to you, you’re not alone. There’s more than £26 billion sitting in lost pensions just now, with the average pot worth more than £9,000.

The good news is you can track down what’s yours. All you need is your National Insurance number and some information about your past employers or pension providers. You can feed that information into the government’s Pension Tracing Service and it can help you find your old plans.

A good way to keep an eye on everything is to have all your pension plans in one place. Not only will it help you keep track of what’s yours, but it could mean less admin and fewer charges.

Want to bring your plans together with us? We’ll do the heavy lifting – and we won’t charge you to do it. Just give us three details about your old plans and we’ll bring them into one place.

Transferring isn’t right for everyone, so check you won’t be giving up any valuable guarantees or benefits first.

-

Already a Standard Life customer?

-

New to Standard Life?

id

The information here is based on our understanding in February 2024 and shouldn’t be taken as financial advice.

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.

Standard Life accepts no responsibility for information in external websites. These are provided for general information.

Related Articles

-

How the gender pension gap affects women

You may have heard of the gender pay gap, but what about the gender pension gap? We examine this phenomenon and what women can do to plan for retirement. MoneyPlus Features Team

MoneyPlus Features TeamJune 30, 2026

Read more6 mins read -

Your top retirement questions answered

Have questions about your pension? You’re not alone. We hear from hundreds of customers each day. Here are the most common questions they ask us.

MoneyPlus Features TeamJune 30, 2026

Read more6 mins read -

Personal pension vs. workplace pension

What’s the difference between personal and workplace pensions, and could having both be an advantage? We explore the best ways to boost retirement savings.

MoneyPlus Features TeamJune 30, 2026

Read more6 mins read