Pensions

Why a bonus sacrifice into your pension plan could mean you keep more of it in the long run

Read our guide to what bonus sacrifice is and the tax benefits you can gain by paying your bonus into your pension plan.

id

Getting a bonus this year? Did you know that paying your bonus into your pension plan could save you on potentially hefty tax and National Insurance (NI) deductions? Here’s why bonus sacrifice could mean you keep more of your bonus and why you might thank yourself later.

id

If you’re lucky enough to get a bonus this year, you might want to consider paying it into your pension plan if you can afford to. Doing this could mean you get to keep more of it, maximise your pension benefits before tax year end and potentially reap the rewards in the years to come.

First let’s take a look at the tax and NI benefits of bonus sacrifice (sometimes called ‘bonus exchange’).

The benefits of bonus sacrifice – in numbers

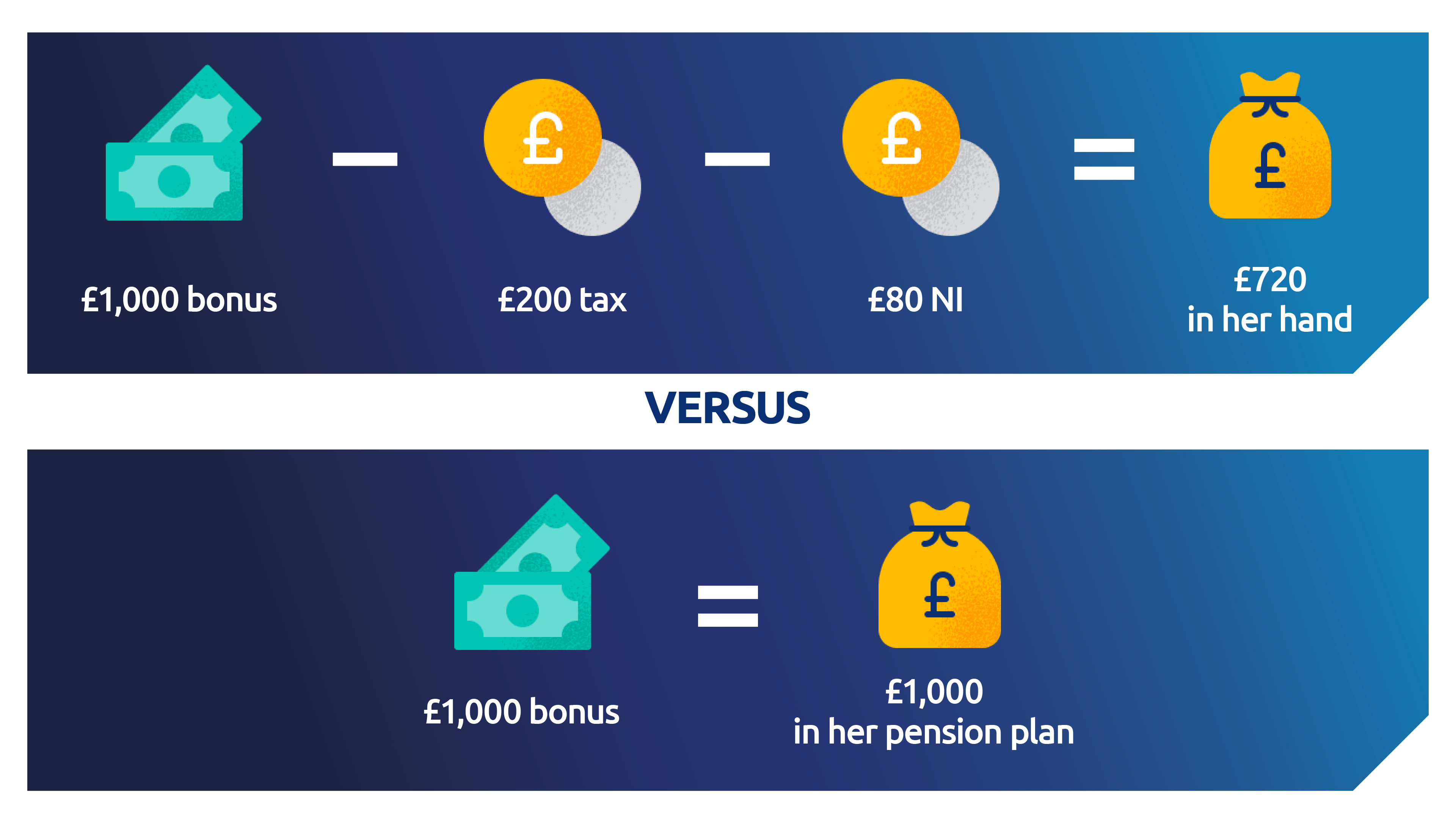

Nicola is a 35-year-old office manager, earning £40,000 a year. She’s due to get a bonus of £1,000 at the end of March.

If she takes all of her bonus in her pay, she’ll pay 20% tax on all of it, as well as 8% NI payments (be aware that these figures apply to the 2024/25 tax year and tax rates are different in Scotland).

But if Nicola opts to use bonus sacrifice to pay all of her bonus into her pension plan, she’ll get the full amount of £1,000 invested.

id

Her employer may also be willing to pass on some of the employer NI payments that may have already been taken from her bonus, which would mean more than £1,000 going into her pension plan. If you pay tax at the higher or additional rate, your tax savings could be even more.

Tax rules and legislation can change, and personal circumstances and where you live in the UK also have an impact on your tax treatment. For example, if you’re a higher or additional-rate taxpayer the amount of tax you pay on a bonus could be much higher.

Don’t underestimate the power of compound growth

Remember your pension plan is invested. Which means you can potentially get additional growth on any investment growth you get from that lump sum. This is thanks to compound growth.

In a nutshell, compound growth is the ‘snowballing’ effect of receiving growth on growth. It means that each year you have the opportunity to achieve growth, not only on the money you’ve invested, but also on the growth you might have already experienced.

As an example, let’s say you have £100 and invest it. Any growth you get is applied to the £100. In the next year though, any growth is applied not only to your original £100, but also to the investment growth that you achieved from that £100. This happens year on year and every year the impact is slowly magnified.

This difference may be small over one year but, given time, compounding can build up significantly. And over longer time periods, it could make a significant difference to the value of your investment, although that’s not guaranteed. And, you don’t pay tax on any of that potential growth while your pension plan is still invested – you only pay tax when you come to take money from it.

Give your pension plan a boost before tax year end

With the end of the tax year fast approaching, now could be the perfect time to use your bonus, or any extra savings you have, to make the most of any tax-free allowances you have left.

For most people the total amount you, your employer or any third party can pay into your pension plan in a tax year without facing a tax charge is £60,000. This is known as the pension annual allowance. If you’ve started taking money from your pension plan already, a reduced allowance known as the Money Purchase Annual Allowance might apply instead.

If you’ve almost used all of your annual allowance for this year, or if you’re worried your bonus will take you over your limit, then it’s worth checking how much you used in the last few years. You might still be able to carry over any unused allowances from the previous three tax years and maximise your pension payments.

How do I sacrifice my bonus into my pension plan?

If you think bonus sacrifice is right for you then first you need to make sure your plan accepts payments from your employer. If it does, then all you need to do is speak to your employer before your bonus is paid and let them know how much you would like to sacrifice. Your employer will then pay some or all of your bonus into your pension plan.

If your plan doesn’t accept employer payments, or if your employer doesn’t offer bonus sacrifice, you can still pay your bonus in to your pension plan after it has been paid to you in the same way you would pay in a single payment. You won’t save on tax and NI deductions this way, but your payment will benefit from pension tax relief.

Next steps

Our pension calculator helps you see if your pension savings are on track for the future you want. Using this simple tool can help you see if any extra payments could help increase the amount you’ll have in the future.

You can keep track of your Standard Life pension plan, including its value, by logging in or registering for online services.

The information here is based on our understanding in March 2025 and shouldn’t be taken as financial advice.

A pension is a long-term investment that you cannot normally access until age 55 (rising to 57 from 6 April 2028). Its value can go down as well as up and may be worth less than was paid in.

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.

Related Articles

-

Your top retirement questions answered

Have questions about your pension? You’re not alone. We hear from hundreds of customers each day. Here are the most common questions they ask us.

MoneyPlus Features TeamJune 30, 2026

Read more6 mins read -

Personal pension vs. workplace pension

What’s the difference between personal and workplace pensions, and could having both be an advantage? We explore the best ways to boost retirement savings.

MoneyPlus Features TeamJune 30, 2026

Read more6 mins read -

How the gender pension gap affects women

You may have heard of the gender pay gap, but what about the gender pension gap? We examine this phenomenon and what women can do to plan for retirement.

MoneyPlus Features TeamJune 30, 2026

Read more6 mins read