Financial Wellness

Why do so many of us feel overwhelmed by pensions?

If half of us feel overwhelmed by the amount of information on pensions, it is little wonder people might lack confidence in making decisions about their retirement. Targeted education and communication is therefore vital.

id

If half of us feel overwhelmed by the amount of information on pensions, it is little wonder people might lack confidence in making decisions about their retirement. Targeted education and communication is therefore vital.

Only a fifth of women have done a great deal of planning or thinking around how much money they need to live on in their retirement. This compares to slightly more than a third (35%) of all men.

Meanwhile, more than a third (36%) of women have done no planning.

And a quarter of women say they don't know how to review their long-term finances, and never check them as a result (compared to 12% of men).

These findings are from our Retirement Voice 2022 report, where for the second year running we surveyed the views of around 6,000 people in the UK from all walks of life .

Of course, it is difficult for us to plan for our retirement if we don’t feel that we understand pensions well enough – and this appears to be part of the problem.

Pension knowledge

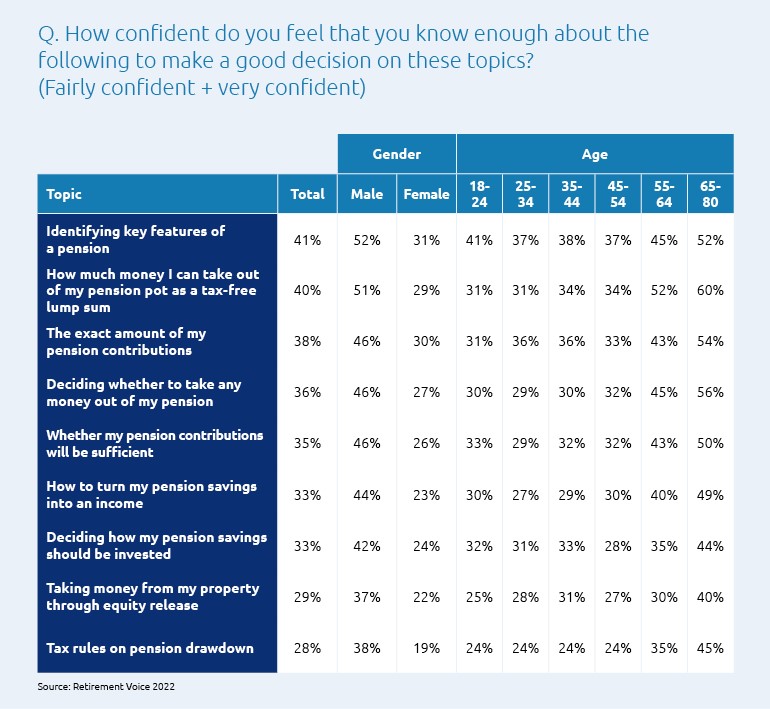

On average, women are a lot less confident that they have enough knowledge of pensions to make good decisions (see Figure 1).

Younger people are also generally less confident. Meanwhile people aged 65–80 are typically the most confident, followed by those aged 55–64.

Figure 1: Women and younger people generally feel less confident in their knowledge of pensions

Feeling overwhelmed?

One the reasons people lack confidence in their knowledge of pensions could be the nature of the information available.

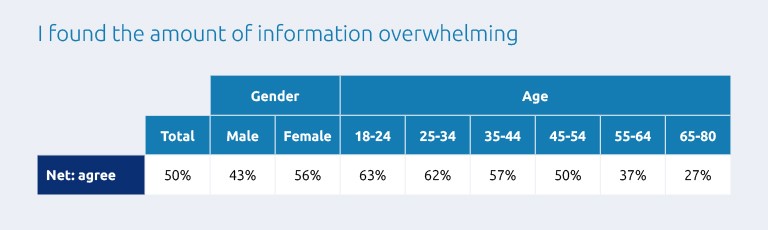

Half of us find the amount of information on retirement planning information “overwhelming”. This proportion is even greater for women and younger generations (see Figure 2).

People aged 18–24 are most likely to feel overwhelmed, followed by the next youngest age groups. Those already retired or closer to retirement feel least overwhelmed.

Figure 2: Many people find pension information overwhelming

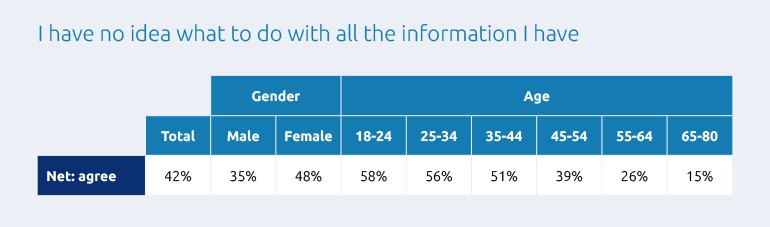

Many people also say they have no idea what to do with the information they have (see Figure 3). Again, people aged 18–24 feel this most often, followed by the next youngest age groups.

Figure 3: Many people don’t know what to do with the pension information they have

This indicates that more effective and readily available financial education could boost many people’s financial planning and overall financial wellness.

So, what information would people find most interesting?

Information needs

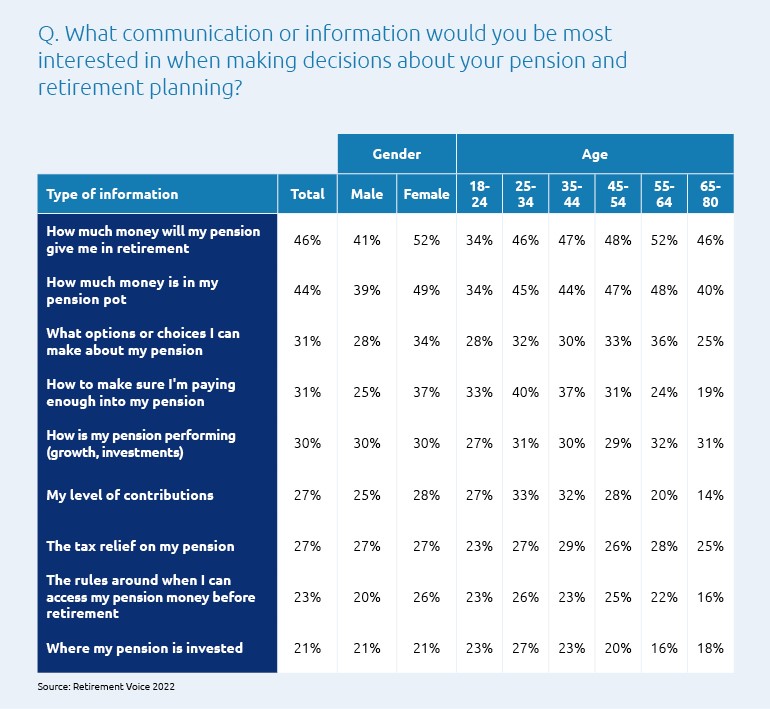

Both women and men are most interested in knowing how much money their pension will give them in retirement, and how much is in their pension pot.

For almost each type of information need, though, women express more of an interest than men (see Figure 4).

Figure 4: People are most interested in knowing the size of their pension, and what it will provide in retirement

Conclusion

Our research indicates that people who do a great deal of planning, or just a little, have a more positive outlook on their future. (See Why retirement planning benefits people of all incomes: survey results to read more on this.)

Yet many people still do no retirement planning, and the nature of the information available on pensions appears to be part of the problem.

Fundamentally, the problems in this article affect all of us to some extent. However, there is clearly value in taking a segmented approach to helping people, as some cohorts need more support than others.

We must therefore continue to tailor the support we offer, particularly to women and younger generations.

Where people access advice and guidance varies. But wherever they turn to, it needs to be personal, relatable, and provided in a simple and engaging way for customers.

Related Articles

-

Inheritance tax changes and pension scams: what employers should know

Learn how employers can support employees during this time. Donna Walsh

Donna WalshJuly 06, 2026

Read more4 mins read -

Rethinking financial wellbeing: from pensions to personal finance

Financial wellbeing is a growing priority for employers. But creating meaningful impact means going beyond pensions and offering practical, relevant support that reflects employees’ day-to-day financial lives. Emma Furlonger

Emma FurlongerJune 01, 2026

Read more5 mins read -

Practical ways to support women’s financial wellbeing at every age

The cost of living and key life events are having a disproportionate impact on women’s finances. Here’s what employers can do to help boost women’s financial wellbeing – whatever life moments they’re facing. Gail Izat

Gail IzatMarch 31, 2026

Read more5 mins read