Financial Wellness

Many of us are under-saving for retirement – say UK government figures

Half of us are projected to have less than a “moderate” pension income in retirement. So it’s vital that new ways are found to encourage people to think more about their long-term savings.

id

Half of us are projected to have less than a “moderate” pension income in retirement. So it’s vital that new ways are found to encourage people to think more about their long-term savings.

Auto-enrolment has been brought back into the spotlight, after the UK government backed legislation to expand savings into workplace pension schemes.

The private members’ bill will give ministers powers to lower the age at which employers must put workers into a pension scheme from 22 to 18.

It also paves the way to abolish the ‘lower earnings limit’ that lets companies make no pension contributions on the first £6,240 of a worker’s income.

Standard Life supports both measures because many people are still not on course for a comfortable retirement – as indicated most recently by government figures released in March 20231.

What does the government data indicate?

The recent government figures indicate that:

• 12% of working-age people (4.1 million) are projected to have a pension income that falls below a Minimum Standard

• 51% of working-age people (17.7 million) are projected to have a pension income below a Moderate Standard

• 88% of working-age people (30.4 million) are projected to have a pension income below a Comfortable Standard

These categories are based on the PLSA’s Retirement Living Standards, which are designed to help people picture the lifestyle they want when they retire and understand what it might cost2.

PLSA Standards are pitched at three different levels3:

• Minimum – which a single person will need about £11,000 a year to achieve

• Moderate – which a single person will need about £21,000 a year to achieve

• Comfortable – which a single person will need about £34,000 a year to achieve

For couples, these collective figures are: £17,000; £31,000; and £50,000, respectively.

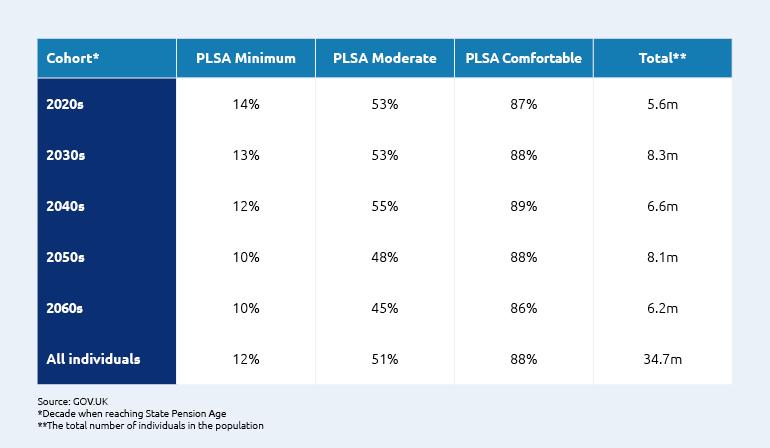

How on track are different generations?

Over time, more people are projected to meet the PLSA Minimum or Moderate Standard. This is partially driven by the State Pension being uprated by triple lock, and more individuals benefitting from being auto-enrolled in workplace pensions.

That said, a larger-than-average proportion of people due to retire in the 2040s are projected to struggle in retirement (see Figure 1).

People in this age group will not have benefitted from a full career of auto-enrolment, and are less likely to have been enrolled in a defined benefit (DB) scheme compared to those approaching retirement in the 2020s. (See the report, Slipping between the cracks? Retirement income prospects for Generation X for more information on this issue.)

Even in the 2060s, though, a large proportion (45%) of people retiring are not projected to meet the PLSA Moderate Standard.

Figure 1: The proportion of working-age people not achieving a moderate retirement standard is projected to increase in the 2040s

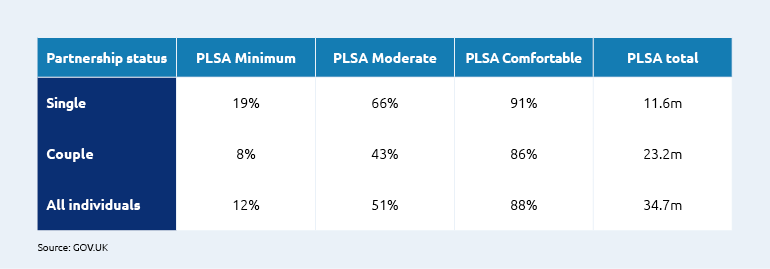

How does relationship status affect retirement preparedness?

Relationship status also appears to be a factor in how likely people are to have a comfortable retirement.

Almost a fifth (19%) of single pensioners are projected to not meet the PLSA Minimum Standard, compared with 8% of pensioners in a couple. This pattern can also be seen when comparing against the PLSA Moderate Standard (66% vs. 43%).

Figure 2: Almost a fifth of single pensioners are projected to not meet the PLSA Minimum Standard

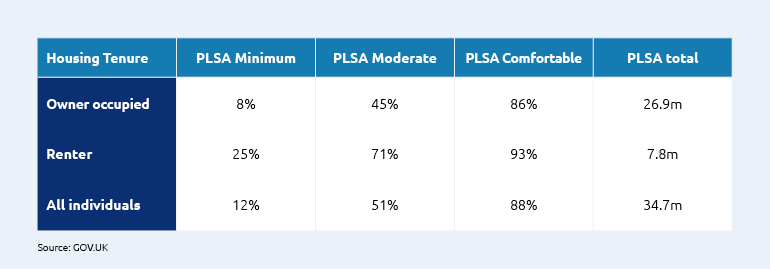

How does property ownership affect retirement preparedness?

When measuring under-saving using the PLSA’s Standards, pension income has been compared after housing costs, as the Standards assume people will be mortgage- and rent-free in retirement. However, of course, this is not always the case.

Housing costs appear to play a significant role in the adequacy of pension incomes, with homeowners facing significantly lower costs.

Twenty-five percent of renters are projected to not meet the PLSA Minimum Standard, compared with 8% of owner occupiers (see Figure 3).

Figure 3: The proportion of working-age people not meeting the PLSA Standard by housing tenure

The model assumes home ownership will continue at similar levels in retirement to existing levels (just under 80%).

However, since the early 1990s there has been a rise in private renting, according to the Joseph Rowntree Foundation.

In 1993, 1-in-10 people of working age rented privately – now it’s a quarter.

Private renting is rising in every age group, but the biggest increases are among people aged between 35 and 44. This group is three times more likely to rent than was the case 20 years ago.

Already, 750,000 people over-60 live in private rented housing in England. And the proportion of households headed by older renters has doubled in the last 15 years.

This trend poses the risk of under-saving (after housing costs have been factored in) increasing for future generations of retirees.

If people find themselves still paying rent or mortgage repayments in retirement, they will need to save considerably more to cover rent throughout retirement in addition to their non-housing costs.

Although state support would be available to some people, in the form of Housing Benefit, this is only available to those on low incomes and may not cover the full cost of private renting.

Next steps

We support the aims of the private members’ bill, as they will help raise retirement savings levels.

Auto-enrolment has normalised regular pension saving largely through inertia. But inertia has its downsides, with many people insufficiently engaged with their long-term savings.

These challenges are compounded by the nature of the support on offer. Just one-fifth of 50–64-year-olds have spoken to a financial adviser about their pension, according to the report A Guiding Hand: Improving access to pensions advice and guidance, produced by the Social Market Foundation and sponsored by Phoenix Group, Standard Life’s parent company.

And just 14% of these people used the government’s Pension Wise service when accessing their pension for the first time.

We therefore need to find ways to harness inertia – such as through auto-escalation of contributions – while also finding new ways to encourage people to think more about their long-term savings. Targeted communication and financial education via the workplace will be a vital part of these efforts.

Standard Life customers can see how their pension savings are projected to measure up against the PLSA Standards by using our retirement calculators and tools on the app or on their online dashboard.

1 There were 34.7 million people included in these government figures. Pension income is calculated as the income from State Pension age onwards, averaged over the whole of retirement.

2 Of course, any assessment of the adequacy of future pension income is complex and involves subjective judgement. What an individual may need, or want, in retirement is dependent on their own individual preferences and expectations. Adequacy measures are also affected by uncertain future economic trends. And estimates can change based on the methodology, the measure used and the assumptions made.

3 The PLSA Standards have recently been updated in January 2023. However, this analysis compares pension income against the 2021 Standards. Although the PLSA Standards have separate Standards for London and outside of London, this government modelling assesses at a national level, and therefore assesses individuals against the outside of London Standards. These estimates are based on State Pension being uprated by the triple lock.

Related Articles

-

Inheritance tax changes and pension scams: what employers should know

Learn how employers can support employees during this time. Donna Walsh

Donna WalshJuly 06, 2026

Read more4 mins read -

Rethinking financial wellbeing: from pensions to personal finance

Financial wellbeing is a growing priority for employers. But creating meaningful impact means going beyond pensions and offering practical, relevant support that reflects employees’ day-to-day financial lives. Emma Furlonger

Emma FurlongerJune 01, 2026

Read more5 mins read -

Practical ways to support women’s financial wellbeing at every age

The cost of living and key life events are having a disproportionate impact on women’s finances. Here’s what employers can do to help boost women’s financial wellbeing – whatever life moments they’re facing. Gail Izat

Gail IzatMarch 31, 2026

Read more5 mins read