Financial Wellness

The gender pension gap – what’s the real cause?

Women in the UK will typically retire with a pension pot about a third of the size of a man’s. This gender pension gap is more than double the gender pay gap.

id

Women typically contribute a larger percentage of their income to their workplace pension than men – until they reach their forties.

Women in the UK will typically retire with a pension pot about a third of the size of a man’s (£51,100 vs. £156,500)1. This gender pension gap is more than double the gender pay gap2.

Women are slightly more willing than men, on average, to contribute to their workplace pension. But under current policies their ability to do so is restricted by their working hours and income, which are the main factors hindering women’s ability to pay into a workplace pension.

In practice, fewer women than men contribute to a workplace pension from the age of 35 onwards.

Standard Life is part of Phoenix Group, this gives us access to Phoenix Insights. These findings are from the report, Caught in a gap – the role of employers in enabling women to build better pensions – produced by Phoenix Insights.

During the first half of their careers, women typically contribute a slightly larger percentage of their income to their pension than men. However, due to differences in average income, women begin to pay less into their pension each month from around the age of 25 onwards.

Overall, the largest difference in the value of men and women’s pension contributions comes at the age of 45–54. This is because of the cumulative effects of broader gender differences, with respect to pregnancy, marriage, divorce, the menopause, and caring responsibilities, among other factors.

Let’s look at these gender differences in more detail.

Participation rates

More men participate in workplace pensions than women. Yet this difference is not large. And, in fact, women are more likely to contribute to a workplace pension – if the impact of different average earnings between men and women is removed3.

The gender difference in earnings is a key factor preventing women from contributing to a pension. For example, women are substantially more likely than men to earn less than the £10,000 threshold for automatic enrolment (AE): 35% of women compared with 11% of men.

Among those whose earnings fall below the AE threshold, however, 54% of women still choose to be a member of their workplace pension scheme, compared to 43% of men. This suggests women value their workplace pension more, despite being on lower incomes.

Conversely, among those not participating in their workplace pension scheme, more men than women have private pensions (other than a workplace pension). This again indicates that women are generally more likely than men to rely on their workplace pension.

Life stages

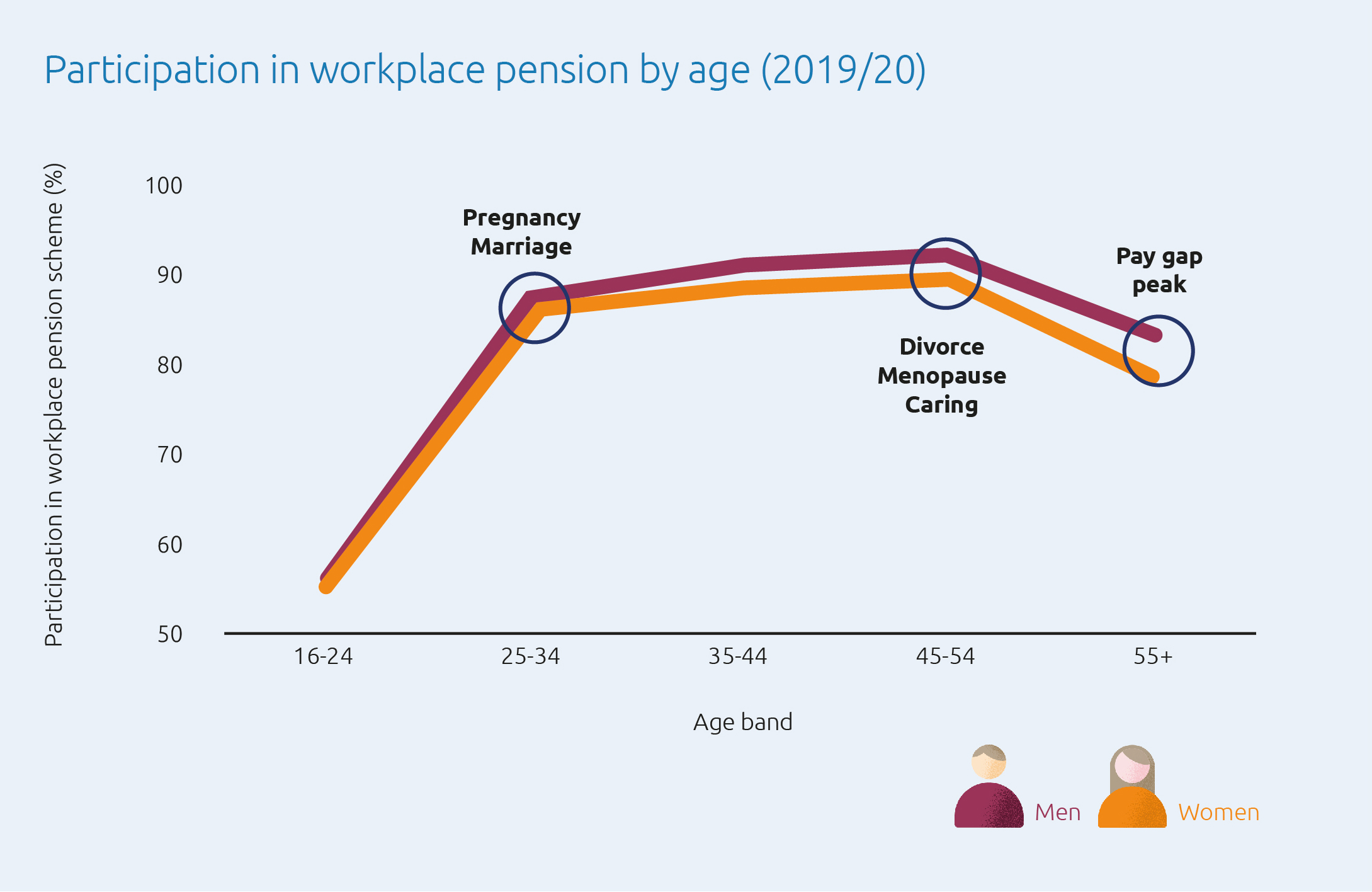

Younger men and women participate similarly in workplace pensions. Participation for both genders rises in parallel to around 85% between the ages of 25 and 34.

However, participation diverges among women and men aged 35–44 (see Figure 1). This is during a time when women are significantly more likely to take on unpaid childcare and household work (particularly among those who are single parents).

Figure 1: The difference in pension participation between men and women is relatively small across all ages

Source: Institute for Employment Studies analysis of Understanding Society

Source: Institute for Employment Studies analysis of Understanding Society

This gender difference in pension participation rates continues for all ages above 35–444. Female participation remains just above 85%, while male participation increases to 91%.

Contribution rates

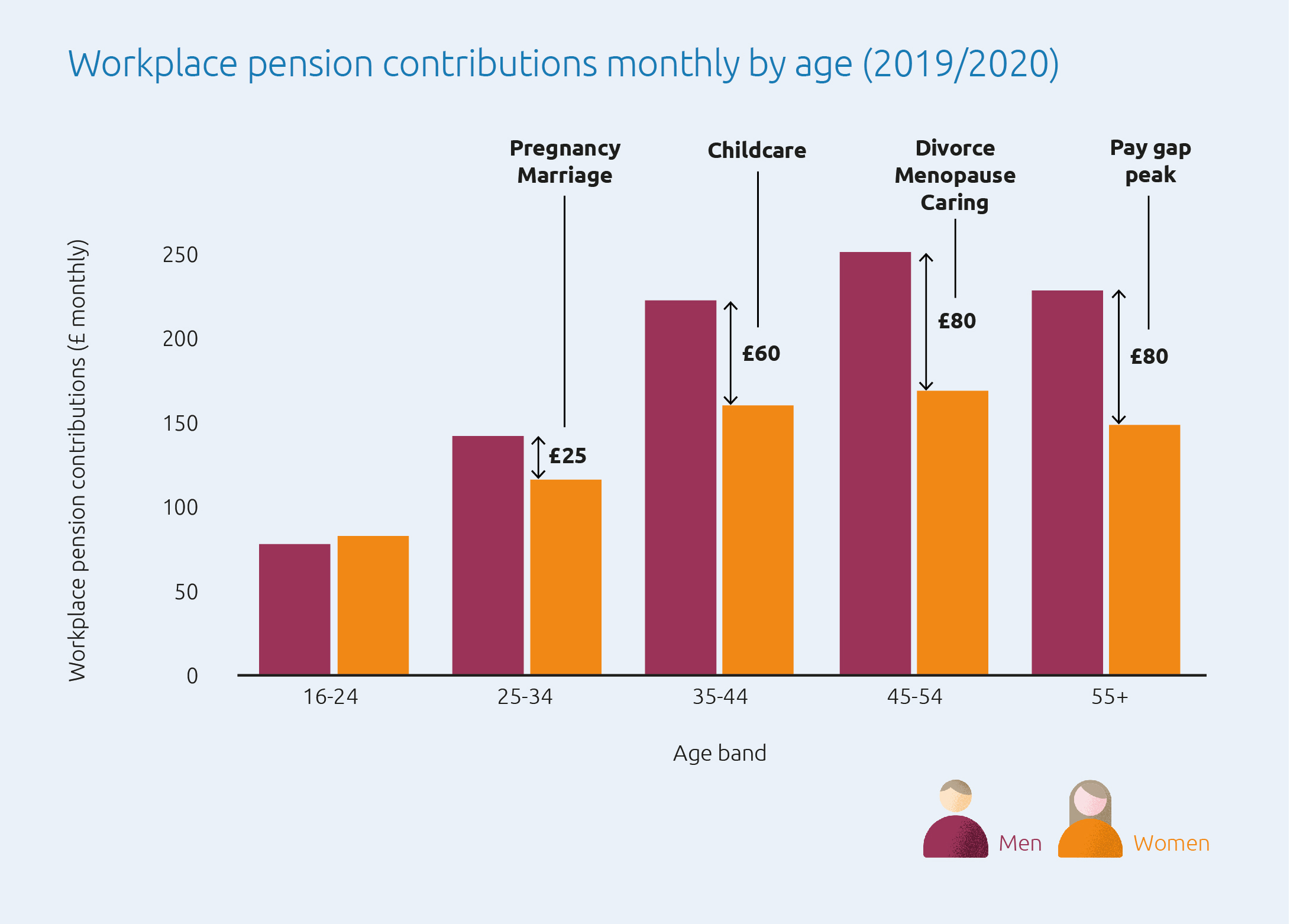

Ultimately, however, the pension gap between men and women is driven by differences in the rate and value of pension contributions.

The value of workplace pension contributions diverges between men and women aged 25–34. This gap then widens with age (see Figure 2).

Men pay considerably more into their pensions each month than women, though this appears to reflect men’s higher earnings.

By the age of 45–54, men are saving around 50% more into their workplace pension than women: £245 compared to £165 per month.

Figure 2: The average monthly contribution gap peaks between the ages of 45 and 54

Source: Institute for Employment Studies analysis of Understanding Society

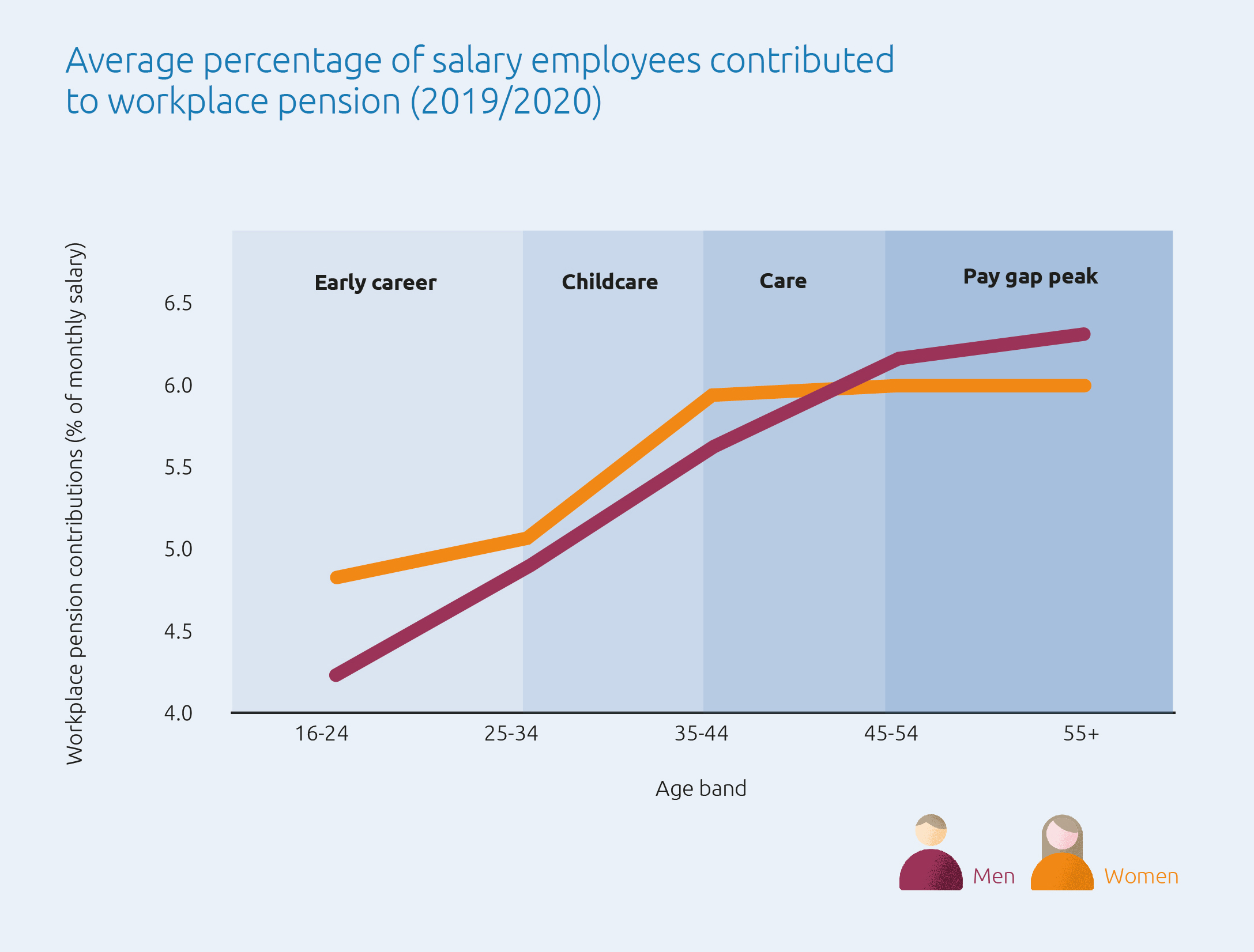

However, the percentage of salary that men and women contribute is roughly equal: standing at around 6% of earnings (see Figure 3).

In fact, women typically contribute a slightly higher percentage of their monthly income into their pension than men until their forties: 6.1% compared to 5.8%, at age 35–44.

Figure 3: Women typically contribute a larger percentage of their monthly income to their pension – until their forties

Source: Institute for Employment Studies analysis of Understanding Society

Why the gap?

The reasons for the gender pay gap are varied, but can broadly be organised within three areas:

1. Unpaid caring and household responsibilities can limit the amount of time available for paid employment. This is made worse by a lack of flexible working in industries where work-life balance is poor. Women carry out 60% more unpaid work (including housework and childcare) than men, found the Office for National Statistics.

2. Occupational segregation whereby women and men are concentrated in different sectors/roles due to social stereotypes and cultural norms, but also linked to opportunities for flexible working.

2. Different pay grades in areas of the workforce with high proportions of women.

Click here to find out how, How employers can help to mitigate the gender pensions gap.

1Facing an unequal future, NOW: Pensions, 2022.

2The gender pension gap is between 34.2% and 40.5%, estimates the Organisation for Economic Co-operation and Development. Meanwhile, the gender pay gap is currently 14.9%, according to the Office for National Statistics.

3This finding also holds when controlling for working hours and a combination of both job hours and income.

4Statistical significance in this case indicates that the relationship between age and workplace pension participation is caused by something other than chance (eg, gender).

Related Articles

-

Inheritance tax changes and pension scams: what employers should know

Learn how employers can support employees during this time. Donna Walsh

Donna WalshJuly 06, 2026

Read more4 mins read -

Rethinking financial wellbeing: from pensions to personal finance

Financial wellbeing is a growing priority for employers. But creating meaningful impact means going beyond pensions and offering practical, relevant support that reflects employees’ day-to-day financial lives. Emma Furlonger

Emma FurlongerJune 01, 2026

Read more5 mins read -

Practical ways to support women’s financial wellbeing at every age

The cost of living and key life events are having a disproportionate impact on women’s finances. Here’s what employers can do to help boost women’s financial wellbeing – whatever life moments they’re facing. Gail Izat

Gail IzatMarch 31, 2026

Read more5 mins read