Annual allowance questions: answered

id

<p class="subtitle">We run regular retirement webinars, where those attending can put their questions to a panel of experts. It’s clear that people want to know more about the pension annual allowance – so retirement expert Scott McQueston is here to answer questions on the topic.

Scott, before we properly start – what is the annual allowance?

It’s the amount that can be paid in across all your pension plans in a tax year before a tax charge applies. It includes your payments into your plan, employer payments, and third-party payments.

The amount is 100% of your ‘relevant UK earnings’ (check out MoneyHelper to get an idea of what this includes), capped at £60,000 gross.

And when I say “£60,000 gross”, that means it includes any basic-rate tax relief that may be added to your pension pot.

Employer payments are not always limited to your relevant UK earnings but are still subject to the annual allowance.

Does the £60,000 apply to everyone?

No. If you earn less than £3,600 or you’re a non-earner, then £3,600 gross will normally be your annual allowance.

High earners could have the tapered annual allowance. This can reduce your allowance to as low as £10,000 per tax year, depending on your earnings. It affects people who have an ‘adjusted income’ of over £260,000. This includes your salary, things like your (and your employer’s) payments into your pension plan, and more. You can find out how you can calculate your adjusted income on GOV.UK.

Can I make payments into my pension plan if I’ve already started accessing my pension money?

Yes. In fact, changes from the Spring Budget that came in on 6 April 2023 may have increased your opportunity to save for retirement.

It’s important to know there’s something called the money purchase annual allowance. Usually, this triggered when you take taxable money from a defined contribution pension plan. For more information on when you might or might not trigger this, check out MoneyHelper.

The money purchase annual allowance was £4,000. But it recently increased to £10,000 per tax year. Keep in mind your relevant UK earnings would need to be at least £10,000 to support this.

The increase means that if you’ve already accessed your pension savings, you can now save more into your pension plan in a given tax year without facing a tax charge. Remember, a pension is an investment and its value can go down as well as up and may be worth less than was paid in.

Does the money purchase annual allowance kick in if I only take my 25% tax-free lump sum?

Not normally, but it depends how you’re taking your money.

Most people can access their pension savings from age 55 (rising to 57 from 6 April 2028). You can normally take 25% of your plan’s value as a tax-free lump sum.

Many of us are working longer these days. But some of us want to, for example, pay off our mortgage early.

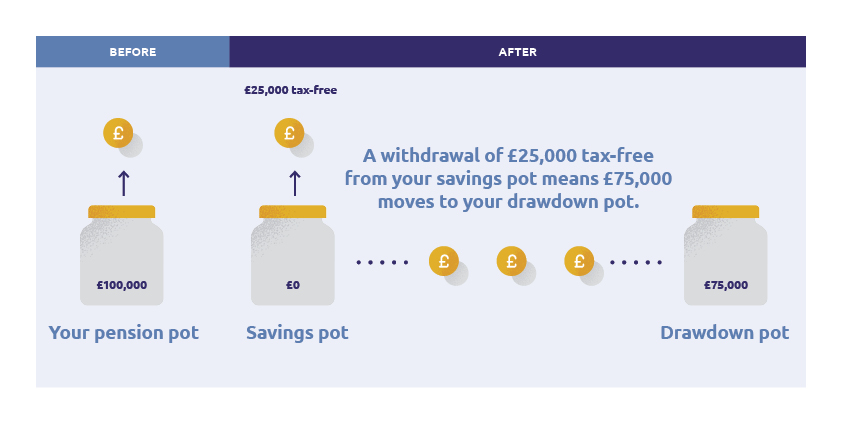

You may have £100,000 in your pension pot at age 55 and take a tax-free lump sum of £25,000 to help with your mortgage.

Let’s say you plan to eventually take the rest as a flexible income (drawdown). If you took £25,000 as a tax-free lump sum, £75,000 would move into a drawdown pot. This means your savings pot will have £0 in it.

id

But you might work for another 20 years and still want to save into your plan. As long as you haven’t touched the money in your drawdown pot, you can normally build up your savings pot again without reducing your annual allowance. You’ll normally be able to have a maximum of £60,000 gross paid into your plan per tax year.

Some people take a guaranteed income for life (annuity). If you take a 25% tax-free lump sum and use the rest to buy a lifetime annuity, you usually won’t trigger the money purchase annual allowance.

Can I take money from my old pension plans without affecting how much I can pay into my current one?

Yes, you normally can as long you’re only taking your tax-free entitlement from your old plan(s).

Or some people take pension pots under ‘small pot rules’. These rules let you take up to three personal pension pots that have a value of less than £10,000 as lump sums – without affecting your annual allowance.

But if you start taking taxable money from your old pension plans, this normally reduces your allowance to £10,000. So if you take pension savings from an old plan via drawdown, you’d affect how much you could save into your current plan.

Don’t forget, the annual allowance applies across all your pension plans.

What counts towards your annual allowance?

All payments – whether that be employer payments, payments from you, or third-party payments – into your pension plans count towards your annual allowance.

When some people pay into their plan, tax relief will be added at the basic rate of 20%. Let’s say this is the case for you and that you want £1,000 paid in. It’d only cost you £800, as £200 would be added as tax relief. So £1,000 gross would count towards your annual allowance.

If you’re a higher or additional-rate taxpayer, you’d need to claim anything over 20% back from the government as this won’t go straight into your pot.

Some people get tax benefits in a different way, like those in a salary sacrifice or salary exchange scheme. And tax relief won’t normally be added on top of employer payments themselves. So in cases like these, what’s been paid can be sort of a “what you see is what you get” situation.

If you want to better understand how the annual allowance could affect you based on your own specific circumstances, it could be worth getting financial advice. If you don’t already have a financial adviser, you can find one at unbiased.co.uk.

Can I use unused allowances from previous years?

Yes, subject to certain conditions.

Before you can carry forward unused allowances from previous tax years, you’ll need to have already used up your annual allowance for the current tax year.

You can only use unused allowances from the last three tax years. And you’ll need to use them from earliest to most recent. Got any unused allowance from three years ago? You’ll need to use that amount of unused allowance first. And you’ll need to have been a member of a pension scheme at that time.

You can use the pension annual allowance tool on GOV.UK to check if you have unused allowances to carry forward.

If you’ve triggered the money purchase annual allowance, you won’t be able to carry forward unused allowances.

If I get tax relief on my pension payments, will I still get this if I carry forward unused allowances?

Yes – a short and snappy answer!

What’s next?

If you’re 50 or over and looking for some support with retirement planning, why not join one of our free webinars? If you’re a Standard Life customer, you can log in online and click the ‘Retirement webinar’ tab for more information. You can find out more about our online services on our website.

The information here is based on our understanding in May 2023 and shouldn’t be taken as financial advice.

A pension is an investment and its value can go down as well as up and may be worth less than was paid in.

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.

Standard Life accepts no responsibility for information in external websites. These are provided for general information.

Related Articles

-

Pensions4 minsSean Young

Pensions4 minsSean YoungWhat happens to my pension savings when I die? Your questions: answered

A retirement expert explains what happens to your pension savings when you die. -

Pensions4 minsMorgan Laing

Pensions4 minsMorgan LaingHow can you take money from a pension plan?

There are a few different ways you can take money from a pension plan. Learn more about your retirement options. -

Pensions4 minsMoneyPlus Features Team

Pensions4 minsMoneyPlus Features TeamSix tips to help boost your pension savings before the end of the tax year 2023/24

There are things you can do before the tax year ends that could potentially benefit you now and in the future. Read our six tips.