Millions left unclaimed in pension tax relief – is some of it yours?

id

Every year, higher-rate and additional-rate taxpayers leave millions of pounds of pension tax relief unclaimed – adding up to £1.3 billion over a five-year period. That’s money that could be in your pocket instead. We explore what pension tax relief is and how you can make sure you’re claiming everything you’re entitled to.

What is pension tax relief?

Pension tax relief is basically the government’s way of giving your pension payments a boost. It’s also the reason why your pension plan is arguably the most tax-efficient way to save for your future. Here’s how it works.

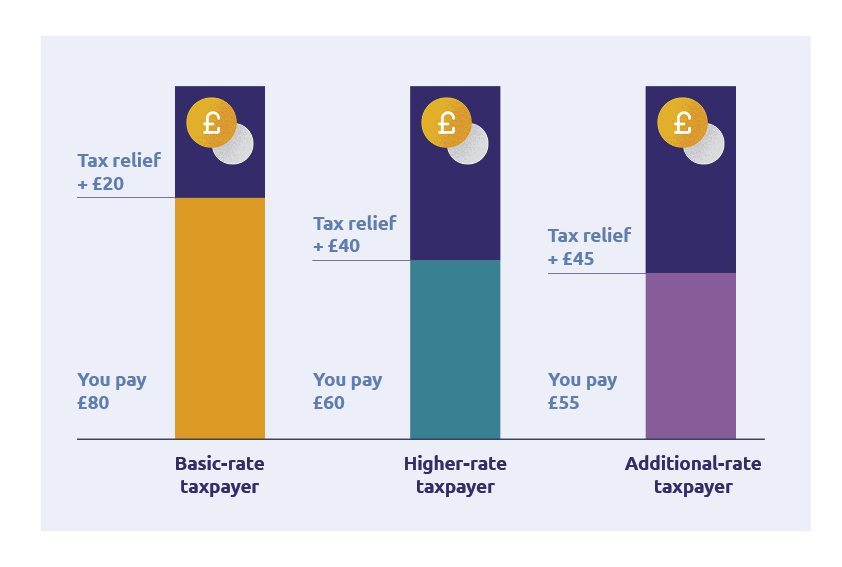

The amount of tax relief you get is based on the rate of income tax you pay. So, let’s say you’re a basic-rate taxpayer and you pay 20% in income tax. This means you’ll effectively get a 20% top-up on your pension payments. So, paying £100 into your pension plan would only actually cost you £80.

If you’re a higher-rate or additional-rate taxpayer who pays 40% or 45% in income tax, it’ll cost you even less. A £100 payment would only cost £60 for a higher-rate taxpayer and £55 for an additional-rate taxpayer.

id

If you don't earn any taxable income, you're still entitled to 20% tax relief on your contributions up to the amount you earn. If have no earnings, or earn less than £3,600 in a tax year, you can still get tax relief on contributions up to £2,880.

Keep in mind that income rates work differently in different parts of the UK.

£1.3 billion left unclaimed

Sound good? If so, you might be wondering why so much is left unclaimed. It’s because tax relief isn’t always automatically applied for higher-rate and additional-rate taxpayers. The process can work slightly differently depending on the type of plan you have or how your employer’s pension scheme is set up.

If you’re in a ‘net pay’ arrangement, you’ll get any tax relief automatically. This is because your pension payment is taken from your salary before you pay any tax. So, you’re effectively getting the tax benefits upfront.

However, if you’re part of a ‘relief at source’ arrangement (which is the case for personal pension plans and some workplace pension plans), then your pension payment is taken from your salary after you pay tax. In this case, basic-rate tax relief (the 20% we mentioned earlier) will be added to your payment by your pension provider and they’ll claim it back from the government. But any higher-rate or additional-rate tax relief needs to be claimed back from the government by you.

This is why there’s over a billion pounds left unclaimed. Many higher and additional-rate taxpayers aren’t claiming the extra 20% or 25% tax relief on top of the 20% basic-rate tax relief. Likely because they don’t know they need to, or maybe because they’re not sure how to.

How to claim back tax relief if you’re a higher or additional-rate taxpayer

First, find out what kind of arrangement you’re a part of. If you’re in a net pay arrangement then you don’t need to do anything. But if you’re part of a relief at source arrangement, here’s what you should do.

To claim your extra tax relief, you’ll need to complete a self-assessment tax return. Or you can also get in touch with the government if you’d prefer. The deadline for online tax returns is 31 January each year, so make sure you keep a reminder in your diary. If you’re doing it through a paper return then the deadline will be earlier: 31 October.

You’ll either get the tax back as a rebate at the end of the year or through an adjustment to your tax code.

Keep in mind the amount of tax relief you’re due could change if you adjust your pension payments or if your salary changes.

Can you claim tax relief for previous years?

You can claim back any tax relief for the last four tax years only.

How much tax relief can you get?

You can only get tax relief on your payments up to your pension annual allowance. For the 2023/24 tax year, this is £60,000 or your total salary – whichever is lower. If you go over this amount, you could face a tax charge.

What’s next?

It could be a good idea to review your pension payments to find out how much tax relief you might be due, or to see whether adjusting your payments could cost you less than you think.

If you’re a Standard Life customer, you can review your payments easily online. You can find out more about our online services on our website, or visit our support page for FAQs and ways to get in touch.

id

The information here is based on our understanding July 2023 and shouldn’t be taken as financial advice.

A pension is an investment and its value can go down as well as up and may be worth less than was paid in.

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay. Laws and tax rules may change in the future.

Related Articles

-

Pensions4 minsSean Young

Pensions4 minsSean YoungWhat happens to my pension savings when I die? Your questions: answered

A retirement expert explains what happens to your pension savings when you die. -

Pensions4 minsMorgan Laing

Pensions4 minsMorgan LaingHow can you take money from a pension plan?

There are a few different ways you can take money from a pension plan. Learn more about your retirement options. -

Pensions4 minsMoneyPlus Features Team

Pensions4 minsMoneyPlus Features TeamSix tips to help boost your pension savings before the end of the tax year 2023/24

There are things you can do before the tax year ends that could potentially benefit you now and in the future. Read our six tips.