How much money can I gift to my children and grandchildren tax free?

id

Understanding how and when to gift money to your children and grandchildren will allow them to fully benefit from your gift without paying more tax than they have to. Find out more about how inheritance tax works and some ways you can gift money as tax efficiently as possible.

id

Life is full of big expenses such as weddings, education fees, paying off debt and getting on the property ladder. So it’s natural that you might want to give your children and grandchildren a helping hand if you can.

Here we’ll cover some of the things you should know about inheritance tax and tax-efficient gifting, including how and when to do it, but inheritance tax can be complicated. So do get professional advice if you’re not sure – there’s likely to be a cost for this.

What do I need to know about tax when I make a gift?

In reality, you can gift as much as you like to your children or grandchildren, but they might have to pay an unexpected tax charge if you don’t think about this when making your plans.

Inheritance tax (IHT) is the main tax to consider if you’re giving away cash.

How does inheritance tax work?

IHT is a tax paid on your estate and certain lifetime gifts after you die.

Your estate typically includes your property, money, possessions and so on, less any outstanding debts you have.

Normally IHT only needs to be paid if the value of your estate is above the £325,000 threshold. And anything above this amount is typically taxed at 40%. So, for example, if your estate is worth £400,000, your beneficiaries would need to pay IHT on £75,000 – meaning they could pay up to £30,000 in tax.

You may also be able to claim up to £175,000 where the family home passes to children or grandchildren. These allowances (totalling up to £500,000) apply to each person, and may be able to be left to a surviving spouse or civil partner. This would give a tax-free threshold of up to £1 million.

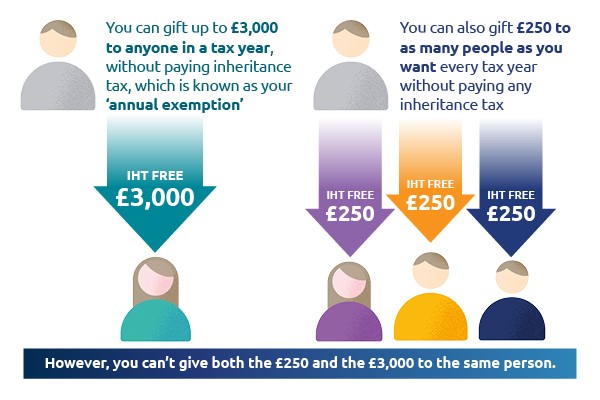

If you’re making gifts during your lifetime, then there’s also your ‘annual exemption’ to think about…

You may also be able to use an exemption for gifts made out of your income which don’t affect your standard of living or cause you to dip into your savings. These gifts would usually need to be regular and you will need to keep records for your executors to prove this.

IHT and gifting

Sometimes a gift you make when you’re alive could be taxed after your death. Broadly speaking, any money you gift over your annual exemption would use some of your £325,000 threshold. This means it could be added to the value of your estate if you don’t live for seven years afterwards. If this happens, the gift would be classed as a 'potentially exempt transfer' and would be taxed based on a scale known as ‘taper relief’.

What is taper relief?

The rate of tax your loved ones will pay on the gift will depend on the amount of time that has passed between you giving the gift and your death. If you die within three years, the value of the gift over the £325,000 threshold will be subject to 40% tax, but the rate of tax due on the gift goes down as more time passes. And normally once seven years have passed, no inheritance tax will be due at all.

| Years between gift and death | Rate of tax on the gift |

|---|---|

| 0 - 3 | 40% |

| 3 - 4 | 32% |

| 4 - 5 | 24% |

| 5 - 6 | 16% |

| 6 - 7 | 8% |

| 7 or more | 0% |

Giving away other assets

Capital gains tax (CGT) is another important tax to consider when gifting. It’s the tax paid on any profit made when you sell (or ‘dispose of’) a non-cash asset or gift that has increased in value. So, for example, property (other than your main home), personal possessions worth £6,000 or more or shares which aren’t in an individual savings account (ISA) or pension plan.

Giving assets away as a gift is currently classed as ‘disposing of an asset’, which means that you may need to pay CGT if you gift an asset like this to a child or grandchild. There is an annual exemption amount of £12,300 of gains (for 2022/23 tax year) before any tax will be due on a gain. These assets will also be subject to the seven-year rule, so IHT and CGT could potentially be payable.

How can I give my children or grandchildren tax-free gifts?

That’s a lot of different types of tax to consider. So to help simplify things, here are some tax-efficient ways to give money to your children and grandchildren.

Give regularly

The £3,000 gift can be carried forward one year but if you don’t use it then, like the £250 every year, you will lose it.

So giving money to your loved ones regularly can be an effective way to minimise the IHT payable on your estate on your death.

Give larger gifts... but be aware of the seven-year rule

If you want to gift larger sums to individuals, these won’t be counted for IHT purposes – as long as you live for seven years afterwards.

If you don’t live for the full seven years, the money you’ve given will be added to the value of your estate. So this means it would use some of your £325,000 threshold. You can't use any inherited threshold or £175,000 family home threshold against lifetime gifts. If you have used all of the available threshold, the gift will be taxed at 40% (although taper relief could reduce this).

Pay into their ISA

You can open a Junior ISA (JISA) for your child, or you can save into to a JISA on your grandchild’s behalf.

You can currently pay up to £9,000 in total in a tax year into a JISA and that money can be invested, which gives it the chance to increase your child or grandchild’s savings over time.

They can access the money when they reach age 18 and they won’t pay any tax on the money they withdraw from the JISA, or pay CGT on any investment growth either.

You could also think about supporting their Lifetime ISA. Depending on their age, giving money to a child or grandchild so that they can save into a Lifetime ISA could help them save for a property or top up their pension savings.

The Lifetime ISA can only be opened between the ages of 18 and 39, so you can’t open it for them. They could save up to £4,000 a year and get a 25% government bonus on top of that.

There are some criteria you need to meet to be able to get a Lifetime ISA which you can read about on Gov.uk.

Gifts to an ISA could be treated as exempt or potentially exempt transfers, depending on their size, how often you make them and if you’ve made them out of spare income.

Think about the benefits of using a trust

Many grandparents may intend to leave some money to their grandchildren in their Will. But what if you’d like to support them financially while you’re still around? Using a trust can help you do this while offering a number of advantages.

As a trustee, you retain an element of control over the funds and how and when they’re paid, while gifts made to the trust can reduce your estate for IHT. Using a discretionary trust gives grandparents the greatest flexibility and control but the taxation is higher and more complex. In particular, while most gifts discussed in this article could be covered by an exemption or be a potentially exempt transfer, a gift to a discretionary trust is a chargeable lifetime transfer and could be subject to IHT at the time the gift is made.

This complexity can be reduced if the trustees choose to invest in an offshore bond as the bond doesn’t generate income. When the funds are needed to meet university costs, for example, bond segments can be assigned to the grandchild. Any chargeable gains which arise after the assignment will be assessed against the grandchild who, as a student, is likely to be a non-taxpayer anyway.

Using an offshore bond within a discretionary trust can provide a good match of control and tax efficiency.

Consider using your pension savings

If you’re aged 55 or over (rising to age 57 in 2028), you can access your pension savings and you’ll usually get 25% of your pot tax free. So you could consider using some of your tax-free lump sum as a gift to your loved ones.

Bear in mind that your pension savings need to last you throughout your retirement, so make sure you’re not giving away anything that you might need to rely on later. Plus, using your pension pot to help out your loved ones doesn’t necessarily have to be done in your lifetime – especially if taking money out now means you won’t have enough left to provide for yourself.

You could also think about nominating a family member as a beneficiary so your pension plan could be passed on to them. Your pension plan isn’t normally included as part of your estate, so your beneficiaries won’t pay any IHT on it, although they could pay income tax on anything they choose to withdraw if you die after the age of 75. This doesn’t apply to all pension plans, so do check with your provider if you’re not sure.

If you’re a Standard Life customer, you can normally update your beneficiary information online or on the app. We will take your wishes into account, although we cannot be bound by them.

Make use of a children's bank account

Ideal for smaller amounts of cash, bank accounts are practical and easy for family and friends to pay money into. And giving younger children access to their savings can help them manage their own money. Just remember that interest earned is usually low and inflation can eat into any returns. Again, any gifts to them will be outside your estate in seven years (unless they are covered by an exemption).

What are the main differences between gifting to a grandchild and gifting to a child?

If a child is getting married, you can give gifts worth up to £2,500 in a year to a grandchild or great-grandchild (on top of your annual exemption). That figure increases to £5,000 if it's your child.

Also, as a grandparent you can't open a JISA for your grandchild – that must be done by the child's parent or legal guardian.

If you’re a parent making a gift to an unmarried child and they are under 18, if that gift earns interest or pays dividends above £100 in any tax year, there are some extra rules. All income from the gift will be taxed as if it were yours. This is to stop parents trying to get a tax break on their own money by using their children’s allowances. This rule doesn’t apply to grandparents or to gifts from parents to their children’s JISAs.

Lots of choice but lots to consider

The good news is that there are many tax-efficient ways you can support your loved ones. And keeping records of your gifts will help your loved ones claim the tax benefits they are entitled to after your death.

But it is a complex area, so it’s well worth seeking advice for your family’s circumstances so that you can make the most of your money, and their future. If you don’t have a financial adviser, you can find one in your local area at unbiased.co.uk. There will likely be a charge for any financial advice you receive.

The information in this article should not be regarded as financial advice.

Pension plans, bonds and some types of ISAs are investments. Their value can go down as well as up and could be worth less than was paid in.

Your own personal circumstances, including where you live in the UK, will have an impact on the tax you pay and laws and tax rules may change in the future.

The information here is based on our understanding in June 2022.

Related Articles

-

Tax3 minsMorgan Laing

Tax3 minsMorgan LaingWhat to think about at the start of the new tax year

The 2024/25 tax year has arrived. Find out what kind of things might impact your finances. -

Tax3 minsKirsty Kerr

Tax3 minsKirsty KerrGetting your child benefit back – and avoiding the tax charge

High earner? Here’s how doing one thing could help you get your child benefit back – and fund your future at the same time. -

Tax4 minsMoneyPlus Features Team

Tax4 minsMoneyPlus Features TeamA simple tax and pensions to-do list for 2024

Follow our to-do list to get your tax and pension plans in order and prepare for the end of the tax year.